Financial Wellness and Productivity: How are your Employees Affected?

Employees worried about their personal finances are less productive, more distracted and are easier targets for poachers. While none of that is a revelation, a recent nationwide survey showed just how pervasive financial insecurity is in the workforce and how large the losses and potential risks are for employers at every level. When asked what they feel stress about, 59% of respondents said personal finances were their number one concern. Other familiar stressors paled in comparison — “my job” at 15%, “relationships” at 12% and “health” at just 10%.

If you have a retirement planning professional who works with your employees, that’s a good start, but the study shows the problem — and effective solutions — go much deeper.

Who’s at Risk?

Not surprisingly, younger, lower-earning employees feel stressed about their finances. But that concern extends all the way up the income ladder and across all generations. In fact, 38% of Millennials reported feeling financial stress, compared to 34% of Gen X and 25% of Baby Boomers.

Employers Impact on Financial Wellness

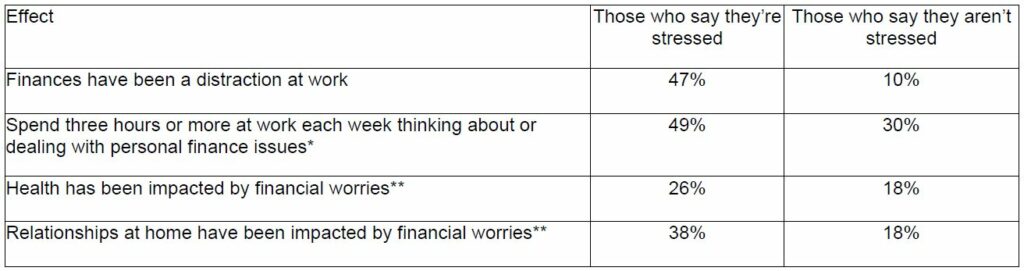

Effects of Financial Stress

For companies concerned about a stressed workforce, financial wellness goes beyond having a retirement plan advisor inform employees about their options and basic financial literacy. Formal coaching on handling personal finances can lower stress, boost productivity and increase retention. Employees who participated in a formal financial wellness plan at work say that it helped them prepare for retirement (47%), pay off debt (29%), save for their goals (29%) and control their spending (29%). Demonstrating concern for employees’ financial health could also reduce the allure of jumping ship if they feel your company cares and is taking steps to help them.

Changes, and not Just in Attitudes

Organizations using retirement plan advisors that offer robust financial wellness programs aren’t just engaging in self-interested risk-abatement – they’re signaling to employees that they understand our economic system is undergoing rapid and significant change. The 20th century paradigm of locking into a lifetime profession has been replaced by seismic shifts and massive uncertainty. Companies that offer employees effective help in navigating the new economy stand to benefit from a workforce that is not only more productive, but one that’s more loyal and committed as well.

For more information on financial wellness and preparing your employees for retirement, reach out to your plan advisor.

*Asked of those who say finances have been a distraction at work

**As noted on page 19 of the study, employees could choose as many answers as applicable to the question, “Which of the following have been impacted by your financial worries?”

- https://www.pwc.com/us/en/industries/private-company-services/library/financial-well-being-retirement-survey.html

- https://www.pwc.com/us/en/private-company-services/publications/assets/pwc-2019-employee-wellness-survey.pdf

Why CFOs Should Consider Partnering with a Retirement Plan Advisor

Many companies are outsourcing more and more activities, mainly because outsourcing can provide cost savings and increase productivity. Outsourcing allows companies to focus more on their core businesses, rather than spending time on areas outside their expertise. For retirement plan sponsors, outsourcing services makes sense for these reasons as well as others.

Reduced Risks

As a plan sponsor, you and your company are plan fiduciaries, and can be held legally responsible for the plan’s administration and performance. Many sponsors outsource some or most responsibility. A 3(21) investment fiduciary assumes part of the risk, functioning as a co-fiduciary that provide prudent and objective advice. A 3(38) investment fiduciary accepts total responsibility and the lion’s share of potential liability for selecting, monitoring and replacing investment options, which helps the plan sponsor manage the risk of legal action concerning investment decisions. A true 3(16) outsourcing of the plan administrator role means offloading not only the day-to-day mechanics of plan administration, but the ultimate fiduciary responsibilities attendant thereto. That said, when plan sponsors contemplate outsourced 3(16) services they need to dive deep into contract review to understand what is actually being outsourced and what might remain in their hands.

Increased Objectivity

Independent third-party plan administration and fiduciary services help your retirement plan by managing conflicts of interest, biases or self-interest. As set out in the Employee Retirement Income Security Act of 1974 (ERISA), both 3(21) and 3(38) investment fiduciaries, as well as 3(16) plan administrators, are required to act solely in the interest of plan participants and must act prudently when making decisions about, or administering, the plan. These actions provide plan sponsors and plan participants with a greater level of risk management and confidence in the retirement plan.

Increased Service Level

Typically, a third-party plan administrator or fiduciary can devote much more time and attention to the support of your retirement plan than can employees. Employees often ‘squeeze in’ plan-related tasks around their regular duties, and may lack the skills, training and resources that an outsourced provider offers.

For more information on outsourcing fiduciary services, contact your plan advisor.

Improve your Retirement Plan by Encouraging Employees to Join

Many organizations face the problem of increasing employee participation in their retirement plans. Participation is crucial to the success of the plan, and it improves employee retention and overall job satisfaction – but how can plan sponsors improve participation rates?

- Design: Your plan needs to meet the needs of your employees and your company. Employee matching contributions, waiting periods for new employees, loan or hardship withdrawal options, investment options, and more should be structured to make it easy for employees to join and feel confident they can control their assets. A qualified consultant can help you understand design features that meets your company and employee goals.

- Communication: Investing and financial markets are confusing for most people, and confusion doesn’t inspire confidence or trust. One way to improve confidence and trust in your plan is to regularly supply plan information and investment education. Communication to employees helps your plan advisors demonstrate their competence and expertise. Consider setting up dedicated meetings, targeted communications, one-on-one sessions, e-mails, webinars, and more! These are just a few ways to communicate the value of your retirement plan to employees and help them prepare for retirement.

For other ideas on how to improve your retirement plan and encourage your employees to participate, reach out to your plan advisor.

Participant Corner: The Importance of Keeping Beneficiary Information Updated

Planning for the departure of a loved one is a difficult thing to think about, but no matter how delicate, it is something any pragmatic planner must consider. What happens to your retirement account when you, your spouse or partner pass? When choosing your retirement plan it’s likely that you were asked to designate a beneficiary – the individual who would receive the money accrued in your retirement account in the event of your passing. As difficult as this may be to think about, it’s always best to be prepared for any contingency. Here are a few tips to consider when updating your beneficiary information.

Take Time to Review Your Account

When reviewing your retirement savings account, take time to consider your designated beneficiaries. This is an important step since retirement account assets typically are not governed by your will. Instead, the assets will pass to the beneficiaries named on the account, which is why it is of utmost importance to keep this information up to date.

Spousal Consent Notice

If you’re married, it is imperative that your spouse’s signature consent is signed in front of a notary public, or your plan administrator, to designate anyone besides your spouse as a beneficiary.

Life Changing Events

Remember to make changes to beneficiaries after any significant life event, including marriage, divorce, birth of a child, or any other milestones. If you’re unsure if something qualifies as a ‘life changing event’, your plan advisor will be happy to assist you. By keeping your beneficiary form up to date, you can ensure that your assets will be distributed as you intended.

As always, planning for retirement and keeping your plan up to date – even in the event of unforeseen adverse situations –is very important. Your plan advisor is here to help you through every step, so make sure to reach out at any time with questions.

This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation.

This newsletter is distributed for general informational purposes only. No part of this newsletter nor the links contained therein is a solicitation or offer to sell investment advisory services. Information throughout this newsletter is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness, accuracy or completeness of this information and the information presented should not be relied upon as such. All investments involve risk of loss, including the possible loss of all amounts invested, and nothing within this newsletter should be construed as a guarantee of any specific outcome or profit. This newsletter is confidential and is intended solely for the information of the person to whom it was delivered and may not be reproduced or redistributed in whole or in part, nor may its contents be disclosed to any other person under any circumstances.