“Time is money. For stocks, the best recipe for loss avoidance is time. The probability of losing money over one day is a little worse than a coin-flip (46%), but the probability declines to just 6% over a 10-year window since 1929.” – Savita Subramanian, Bank of America Head of U.S. Equity and Quantitative Strategy

Review

During the first quarter investors became familiar with new investment terms such as “Reddit traders” and “meme stocks.” Reddit is an online discussion forum where individuals can submit and share content on a wide variety of topics. The subreddit community known as WallStreetBets became widely known for leading the investment craze in meme stocks such as GameStop and AMC Entertainment. Investors also were confronted with the concept of a non-fungible token (NFT). An NFT is a unit of data on a digital ledger called a blockchain, where each NFT can represent a unique digital item. NFT’s can represent digital files such as art, audio, video, and other forms of creative work. Recently, Christie’s Auction House auctioned off an NFT attached to a digital image for $69 million! Even with the headline grabbing new investment themes, the general stock market experienced solid results during the first quarter.

For the first three months of 2021, the S&P 500 Index was up 5.77%. The Dow Jones Industrial Average (DJIA) also performed well as it was up 7.76%. The NASDAQ Composite was up only 2.95% as technology stocks lagged during the quarter. One of the best performing indexes during the first quarter was the Russell 2000, a measure of the small-cap sector of the market, which was up 12.44%. Smaller companies often experience much larger swings in earnings than big companies and have rebounded strongly with the expectation of a reopening economy. Overall, during the first quarter we saw last year’s best performing stocks tended to be the laggards while the worst performers last year have performed well this year.

The top performing sectors of the market during the first quarter were Energy and Financials, while the weakest sectors were Consumer Staples and Technology. Government bond yields climbed, with the 10-year U.S. Treasury note increasing from 0.91% at the beginning of the year to over 1.75% during the quarter. Many analysts expect the 10-year yield to approach 2% at some point this year. The rise in Treasury yields means future cash flows become less valuable relative to their current level which has negatively impacted higher valued technology stocks frequently found in the NASDAQ index. Since the NASDAQ reached its record high on February 12th, growth stocks have largely struggled while other sectors such as financials and energy have rebounded strongly. Financial stocks in general, and most notably banks, should benefit from higher interest rates and a steeper yield curve, while energy stocks have risen as investors expect an increase in oil demand as the economy recovers.

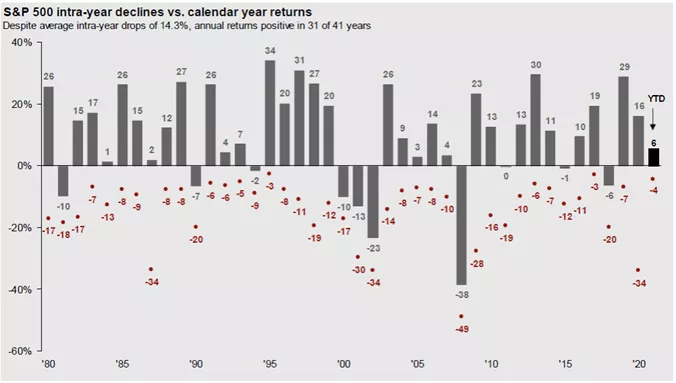

The DJIA, S&P 500, and NASDAQ indices set all-time highs at various times during the first quarter. However, at one point during the quarter the NASDAQ had declined more than 10% from its all-time high. This “correction” is not uncommon, as we have mentioned many times before in our quarterly updates. The red dots in the chart below show the intra-year declines for the S&P 500 since 1980. Over half of the years experienced declines of at least 10% from the intra-year peak, with 15 years posting a drop of 15% or more. Despite the average intra-year drop of over 14% per year since 1980, the annual returns were positive for 31 out of the last 41 years, or about 75% of the time.

One of the lessons from the chart above is for investors to avoid getting scared out of stocks due to short-term pullbacks, and to remain in the stock market for long periods of time to increase the likelihood of solid long-term returns. A prime example would be the large decline in the market during the first quarter of 2020, only to be followed by a strong 12-month return through this quarter, as can be seen in this quarterly report for clients who have been with us for at least a year.

Outlook

A combination of factors should lead to unprecedented levels of economic growth. Those factors include trillions of dollars of fiscal stimulus provided over the last year, expected additional stimulus, continuation of low interest rates, and expectation of a re-opening economy over the rest of the year. Some analysts are now predicting our economy will grow faster than China’s economy this year. Goldman Sachs has one of the most bullish projections with gross domestic product (GDP) growth expectations of 7-8% for 2021 and an unemployment rate of 4% at the end of 2021. The Federal Reserve recently projected U.S. GDP growth of 6.5% for 2021.

Much of the anticipated growth in 2021 will come from consumer spending. Americans are sitting on a large amount of cash which recently increased with another round of stimulus checks for many Americans. In 2020, sales of previously owned homes surged to their highest level in 14 years, and most economists are forecasting sales to rise again this year. It is estimated that consumers who own homes gained $1.5 trillion in equity in 2020 due to the strong appreciation in the real estate market. According to a recent report by The Federal Reserve, household net worth increased to $122.9 trillion in the fourth quarter of 2020 versus $111.4 trillion at the end of 2019.

The New York Federal Reserve latest survey of consumers shows Americans are anticipating higher inflation. The inflation readings for this year are now going to be compared to the same period a year ago when prices were falling during the early stages of the Covid-19 pandemic. With the widespread rollout of vaccinations and the extraordinary government spending over the past year, economists have been lifting their inflation estimates. The Federal Reserve recently projected inflation will increase to 2.4% this year, but then settle at 2% in 2022.

During the next several months there will be much discussion about two large spending packages that might approach $4 trillion in total. The spending will likely target infrastructure, health care, education, and child-care initiatives. The Biden Administration is expected to propose $3 trillion in tax hikes for individuals and corporations to offset most of the proposed spending. Details have not been released for the proposed tax increase for individuals, but we know the Biden administration has proposed increasing the corporate tax rate to 28% from its current rate of 21%. Goldman Sachs market strategist, David Kostin, projects an increase in the corporate tax rate to 25% is more likely than the proposed 28%. Goldman Sachs also projects a decrease of 3% in the earnings for the S&P 500 Index if the corporate tax rate is increased to 25%, and a 9% decrease in earnings if the corporate tax rate is increased to 28%. We will be closely following the developments as the final details will impact the future earnings of the companies in which we invest.

Several recent developments foreshadowing more growth in the future were the Institute for Supply Management (ISM) manufacturing index that jumped to 64.7% in March, which was the highest reading it has had since 1983. Also, the recent jobs report released on April 2nd showed 916,000 jobs added to the economy in March and the unemployment rate falling to 6% as the economy continues to reopen. Large job gains were seen in hard-hit industries such as leisure and hospitality, construction, and manufacturing.

Future developments to monitor as the year progresses include the following:

- Will corporate earnings reports during the year contain the strong anticipated growth rates that are now projected?

- Will the enormous amount of cash currently held by investors continue to be deployed into stocks?

- Will employment continue to strengthen, thus bolstering the consumer’s position to spend on various products and services?

- Will the general economic conditions to which investors have become accustomed remain in place, notably strong growth and accommodative monetary policy by the Federal Reserve?

- Will interest rates stay near historical lows and inflation remain subdued?

Sincerely,

Marietta Wealth Management, LLC