It’s That Time Again! Back-to-School for Fiduciaries

Morgan Davis, Plan Advisor

Can you hear the bells ringing? It’s that time of year to review your to-do list of fiduciary responsibilities. Ask yourself the following questions to make sure you are on top of your responsibilities and liabilities.

- Are you practicing procedural prudence when making plan management decisions?

- Do you clearly understand the Department of Labor’s (DOL) TIPS on selecting and monitoring your QDIA in order to obtain fiduciary protection?

- Are you documenting each plan management decision and its support?

- Are you familiar with current trends in fiduciary litigation?

- Are you certain that your plan is being administered in accordance with your plan document provisions?

- What fiduciary liability mitigation strategies are you following? (Fiduciaries are personally financially responsible for any fiduciary breaches that disadvantage participants.)

- Are you kept abreast of regulatory changes?

- Are you appropriately determining reasonableness of plan fees, services and investment opportunities?

- How do you define “success” for your plan and what metrics do you use to track progress?

- Is your current plan design communicating the appropriate messaging to encourage success for your participants and plan fiduciaries?

- Is your menu efficiently designed for benefit of participants and plan fiduciaries?

- Are you certain you are providing all required communications and distributions to plan participants (including former participants with account balances)?

- Are you handling missing participants appropriately?

- Are you appropriately monitoring and documenting your fiduciary activities and those of your service providers?

- Are you maintaining plan records appropriately?

Many fiduciaries are unaware of their fiduciary responsibilities or do not understand them. If you need help uncovering the answers to any of these important questions, do not hesitate to reach out to your financial professional

About the Author, Morgan Davis

Morgan is responsible for guiding plan sponsors through the intricacies of investment analysis and innovative plan design and making it easy to understand. Blending employer and employee objectives, Morgan encourages plan design initiatives to create optimal retirement plan outcomes for participants. Morgan is a graduate of Michigan State University where she earned a Bachelor of Arts in marketing.

Collective Investment Trusts — The Fastest Growing Investment Vehicle Within 401(k) Plans

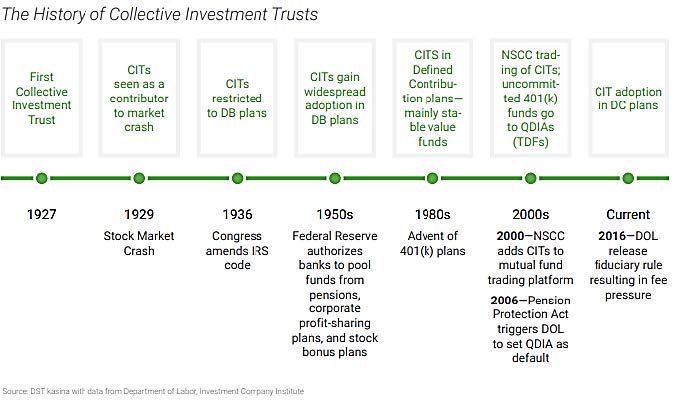

For almost a century, collective investment trusts (CITs) have played an important role in the markets. They were originally introduced in 1927. According to a 2020 study, they are now used in more than 70 percent of plans.¹

For the vast majority of their existence, CITs were available only in defined benefit (DB) plans. In 1936, CIT use expanded in DB plans when Congress amended the Internal Revenue Code to provide tax-exempt (deferred) status to CITs. CITs then gained widespread adoption in the 1950s when the Federal Reserve authorized banks to pool together funds from pensions, corporate profit-sharing plans and stock bonus plans. The IRS also granted these plans tax-exempt status.

In the 1980s, 401(k) plans became primary retirement plans and mutual funds became the primary investment vehicle, due to daily valuation. In the 2000s, CITs gained significant traction in defined contribution (DC) plans due to increased ease of use, daily valuation and availability. During this time, CITs were also named as a type of investment that qualifies as a qualified default investment alternative (QDIA) under the Pension Protection Act of 2006.

From 2011 to 2018, total assets in CITs grew by approximately 64 percent. During which their share of 401(k) assets reached nearly 28 percent, or approximately $1.5 trillion.2

The advantages of CITs are plentiful:

- Lower operational and marketing expenses

- A more controlled trading structure compared to mutual funds

- They’re exempt from registration with SEC, thereby avoiding costly registration fees

On the other hand, CITs are only available to qualified retirement plans and they may have higher minimum investment requirements.

While CITs have traditionally only been available to large and mega-sized plans, continued fee litigation – as well as increased CIT transparency, reporting capabilities and enhanced awareness – has amplified the allure of CITs to plan sponsors across all plan sizes. However, CITs have not been widely available to all plans — until now.

Through your advisor’s strategic partnership with RPAG, a national alliance of advisors with over 60,000 plans and $600 billion in retirement plan assets collectively⁴, they can provide their clients with exclusive access to actively managed, passively managed and target date CITs, featuring top-tier asset managers⁵ at a substantially reduced cost.

For more information on CITs, contact your financial professional.

¹Callan-2020-DC-Trends-Survey

²Collective Investment Trusts: An Important Piece in the retirement Planning Puzzle-Wilmington Trust-2020

³DST kasina with data from Department of Labor, Investment Company Institute.

⁴As of 1/1/2020.

⁵Top-tier asset managers include BlackRock, Franklin Templeton and Lord Abbett.

The target date is the approximate date when investors plan on withdrawing their money. Generally, the asset allocation of each fund will change on an annual basis with the asset allocation becoming more conservative as the fund nears target retirement date. The principal value of the funds is not guaranteed at any time including at and after the target date.

Collective investment trusts available only to qualified plans and governmental 457(b) plans. They are not mutual funds and are not registered with the Securities and Exchange Commission.

Allowable Plan Expenses: Can the Plan Pay?

The payment of expenses by an ERISA plan (401(k), defined benefit plan, money purchase plan, etc.) out of plan assets is subject to ERISA’s fiduciary rules. The “exclusive benefit rule” requires a plan’s assets be used exclusively for providing benefits. ERISA also imposes upon fiduciaries the duty to defray reasonable expenses of plan administration. General principles of allowable expenses include the following:

- The expenses must be necessary for the administration of the plan.

- The plan’s document and trust agreement must permit use of plan assets for payment of expenses.

- The expenses must be reasonable and incurred primarily for the benefit of participants/beneficiaries.

- The expense cannot be the result of a transaction that is a prohibited transaction under ERISA, or it must qualify under an exemption from the prohibited transaction rules.

In light of today’s plan fee environment, it is incumbent upon fiduciaries to request full disclosure of fees and expenses, how they breakdown with services provided, as well as a request for full explanation of who will be the recipient of fees. Ultimately, the ability to pay expenses from a plan trust is a facts and circumstances determination that needs to be made by plan fiduciaries. Because it is possible that the DOL may challenge such determinations it is important that fiduciaries consult ERISA counsel prior to paying questionable expenses from a plan trust and document the decision and reasoning.

For more information on this topic, contact your financial professional.

Participant Corner: Retirement Plan Check-Up

This month’s employee memo encourages employees to conduct a regular examination of their retirement plan to determine whether any changes need to be made. Download the memo from your Fiduciary Briefcase at fiduciarybriefcase.com.

Please see an excerpt below. It is important to conduct regular check-ups on your retirement plan to make sure you are on track to reach your retirement goals. Below are a few questions to ask yourself, at least annually, to see if (and how) they affect your retirement planning.

- Review the Past Year

Did you receive a raise or inheritance?

If yes, you may want to increase your contributions.

Did you get married or divorced?

If yes, you may need to change your beneficiary form.

Are you contributing the maximum amount allowed by the IRS?

In 2020, you can contribute up to $19,500 ($26,000 for employees age 50 or older).

Did you change jobs and still have retirement money with your previous employer?

You may be able to consolidate your assets with your current plan. (Ask your human resources department for more details.) - Set a Goal

What do you want your retirement to look like? Do you want to travel? Will retirement be an opportunity to turn a hobby into a part-time business? Will you enjoy simple or extravagant entertainment?

Take time to map out your specific goals for retirement. Participants that set a retirement goal today, feel more confident about having a financially independent retirement down the road. - Gauge Your Risk Tolerance

Understanding how comfortable you are with investment risk can help you determine what kind of allocation strategy makes the most sense for you. Remember, over time, and as your life changes, so will your risk tolerance. - Ask for Help

If you have questions about your retirement plan or are unsure of how to go about saving for retirement, ask for help. Your financial professional can help you evaluate your progress with your retirement goals, determine how much you should be saving and decide which investment choices are suitable for you.

For more information on reaching your retirement plan goals, contact your plan’s financial professional.

Using asset allocation as part of your investment strategy neither assures nor guarantees better performance and cannot protect against loss of principal due to changing market conditions.

This material was created to provide accurate and reliable information on the subjects covered but should not be regarded as a complete analysis of these subjects. It is not intended to provide specific legal, tax or other professional advice. The services of an appropriate professional should be sought regarding your individual situation.

The material presented was created by an outside vendor (or third party).

This newsletter is distributed for general informational purposes only. No part of this newsletter nor the links contained therein is a solicitation or offer to sell investment advisory services. Information throughout this newsletter is obtained from sources which we believe reliable, but we do not warrant or guarantee the timeliness, accuracy or completeness of this information and the information presented should not be relied upon as such. All investments involve risk of loss, including the possible loss of all amounts invested, and nothing within this newsletter should be construed as a guarantee of any specific outcome or profit. This newsletter is confidential and is intended solely for the information of the person to whom it was delivered and may not be reproduced or redistributed in whole or in part, nor may its contents be disclosed to any other person under any circumstances.